Best mortgage lenders of April 2024

“Verified by an expert” means that this article has been thoroughly reviewed and evaluated for accuracy.

BLUEPRINT

Updated 5:14 p.m. UTC April 8, 2024

Editorial Note: Blueprint may earn a commission from affiliate partner links featured here on our site. This commission does not influence our editors' opinions or evaluations. Please view our full advertiser disclosure policy.

Comparing the best mortgage lenders of 2024 can help you find a home loan with a competitive rate and term. Many of these lenders offer home loans with flexible down payment and income requirements that can benefit homebuyers who struggle to qualify for a traditional mortgage.

We’ve ranked both traditional and online lenders using several factors — including whether the lowest rate is higher or lower than the national average, fees, potential discounts, borrower eligibility, customer experience and the ease of the application process.

Best mortgage lenders

- Ally: Best on a budget.

- Better: Best for FHA loans.

- Bank of America: Best for closing cost assistance.

- USAA: Best for low origination fees.

- Veterans United: Best for VA loans.

- New American Funding: Best for custom mortgages.

- Chase: Best for discounts.

- SoFi: Best for quick closings.

- Navy Federal Credit Union: Best for military.

- Wells Fargo: Best for thin credit.

Why trust our mortgage experts

Our team of experts evaluated hundreds of mortgage products and analyzed thousands of data points to help you find the best fit for your situation. We use a data-driven methodology to determine each rating. Advertisers do not influence our editorial content. You can read more about our methodology below.

- 18 mortgage lenders reviewed.

- 180 data points analyzed.

- 6-stage fact-checking process.

Ally

Better

Bank of America

USAA

Veterans United

New American Funding

Chase

SoFi

Navy Federal Credit Union

Wells Fargo

Compare the best mortgage lenders

| LENDER | MINIMUM RATE | MAX DTI RATIO | TIME TO CLOSE |

|---|---|---|---|

Ally

| Above national average

| 50%

| Few weeks to a few months

|

Better

| Below national average

| 50%

| 30 to 45 days

|

Bank of America

| Above national average

| No maximum

| 4 to 6 weeks

|

USAA

| Below national average

| Up to 50%

| 30 to 45 days

|

Veterans United

| Below national average

| Does not disclose

| 40 to 50 days

|

New American Funding

| Below national average

| Up to 45%

| 14 to 30 days

|

Chase

| Below national average

| 43%

| 3 weeks

|

SoFi

| Below national average

| Up to 50%

| Usually within 30 days

|

Navy Federal Credit Union

| Below national average

| Does not disclose

| 30 to 45 days

|

Wells Fargo

| Below national average

| Does not disclose

| 30 to 90 days

|

Methodology

Our expert writers and editors have reviewed and researched multiple lenders to help you find the best mortgage. Out of all the lenders considered, the seven that made our list excelled in areas across the following categories (with weightings): loan cost (30%), eligibility and accessibility (20%), customer service (20%) and ease of application (30%).

Within each major category, we considered several characteristics, including minimum APR, maximum allowed debt-to-income (DTI) ratio, minimum credit score requirements and applicable fees. We also evaluated each provider’s customer support options, borrower perks and features that simplify the borrowing process—like time to close and preapproval time.

Why some lenders didn’t make the cut

Of the mortgage lenders that we reviewed, only a fraction made the cut. The lenders that didn’t have high enough scores to be included received lower ratings mostly due to having a lack of transparency around credit score and DTI ratio requirements as well as preapproval and closing timelines. Some of the excluded lenders also had limited customer service options and bad customer reviews.

More millennial households own than rent: Here’s where they’re buying.

Real estate: Vacation home sales are down

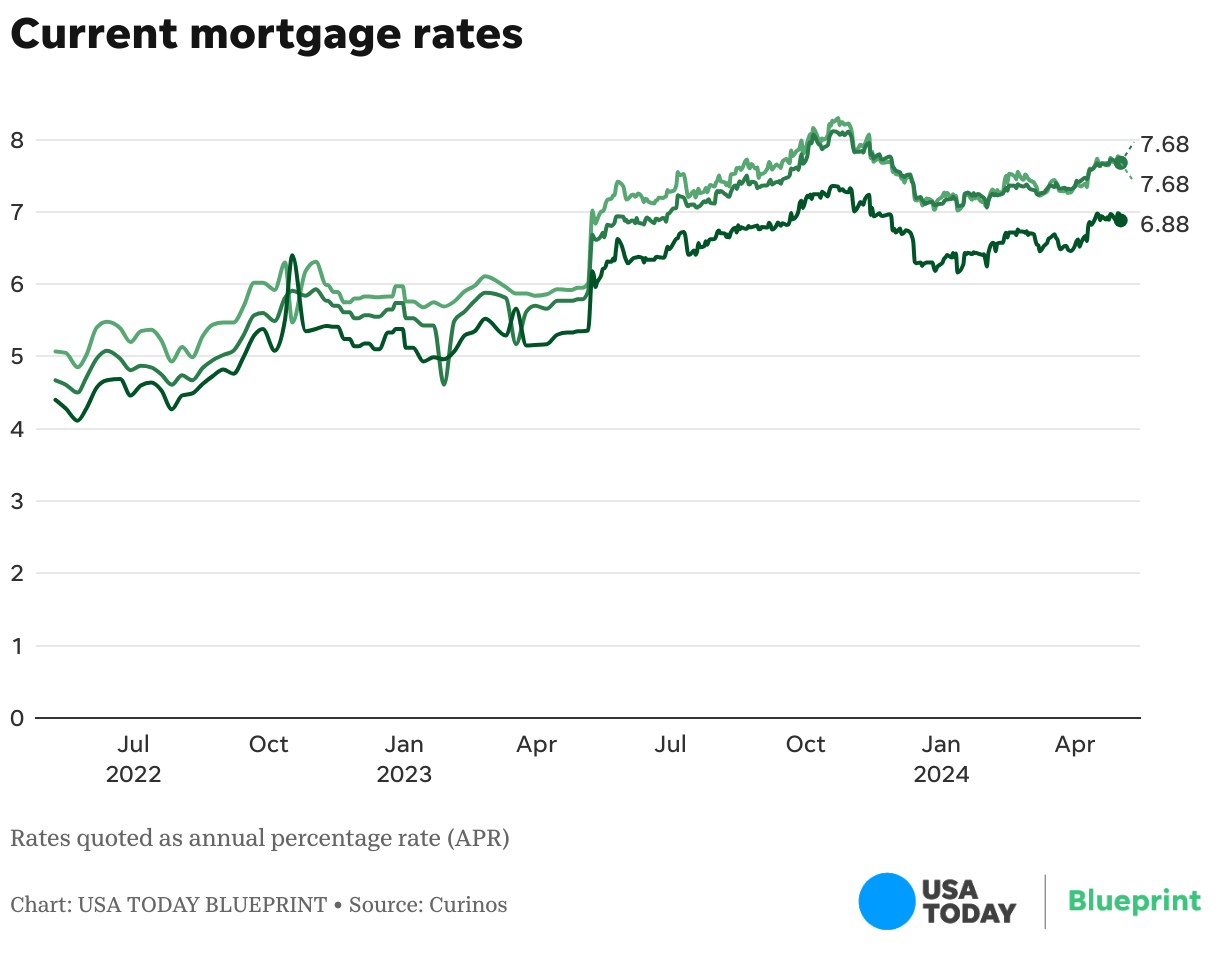

Current mortgage rates

Mortgage rates are constantly fluctuating, so it’s a good idea to check them regularly when you’re preparing to take out a mortgage. Here are the current mortgage rates to give you an idea of what to expect as you compare your options.

Mortgage rates forecast for 2024

The Federal Reserve has hiked the federal funds rate 11 times since March 2022 in an effort to combat inflation. As a result, mortgage lenders have increased their rates to generational highs, which has impacted the purchasing power of both first-time and repeat homebuyers.

Experts expect mortgage interest rates to peak near 7% or even 8% in 2024 before gradually trending lower — possibly landing between 5% to 6% before the end of the year. However, what will happen will ultimately depend on the future actions of the Fed and how fast rates might drop if the Fed’s current trend of higher-for-longer rates reverses.

What is a mortgage and how does it work?

A mortgage finances a home purchase and is repaid over a specified number of years through monthly payments. Most home loans have a repayment period from 10 to 30 years and a fixed interest rate.

Your interest rate depends on several factors including your loan term, mortgage type and credit history. You will keep the same rate, term and monthly payment unless you decide to apply for a mortgage refinance and replace your existing loan.

Borrowers with a fixed-rate mortgage enjoy the same monthly payment amount for the life of the loan. As the remaining loan balance decreases, more of the payment reduces the principal as less interest accrues.

Longer-term mortgages, such as a 30-year term, have the lowest monthly payments but your total interest costs are higher than shorter terms as it takes longer to pay off the loan.

In contrast, shorter terms, like a 15-year mortgage, usually have less total interest and better interest rates although your monthly payment is higher due to the more aggressive payoff date.

Different types of mortgages

There are several different types of mortgages you can apply. Any of these loans can help you buy a home, but there are different borrower requirements, interest rate types and fees.

Here are the different types of mortgages:

- Conventional mortgage: A non-government loan issued by a private lender. This loan can have lower fees than federally-backed loans. Additionally, most are conforming loans with county-specific loan limits set by the Federal Housing Finance Agency (FHFA) and have lower interest rates than non-conforming loans.

- Fixed-rate mortgage: A home loan with the same interest rate and monthly payment for the life of the loan. Borrowers follow an amortization schedule with a repayment period from 10 to 30 years.

- Adjustable-rate mortgage (ARM): Also known as a variable-rate mortgage, this product typically has a fixed interest rate for an introductory period of several years. Next, it switches to a variable rate that can adjust up or down at defined increments. Your monthly payment fluctuates as rates change but it can be a more affordable loan type for homeowners planning to sell in a few years.

- Jumbo loan: A non-conforming loan to buy properties exceeding the conforming loan limit. This option is more common in high-cost housing markets. The interest rate is usually higher than conforming loans.

- FHA loan: Backed by the Federal Housing Administration (FHA), this loan has more lenient credit and down payment requirements than conventional mortgages. Lenders may only require a minimum 580 credit score and a 3.5% down payment. However, mortgage insurance premiums can apply for the entire repayment period.

- VA loan: The U.S. Department of Veterans Affairs (VA) insures home loans to eligible service members, veterans and spouses. A VA-backed purchase loan doesn’t require a down payment or mortgage insurance, although a one-time funding fee applies.

- USDA loan: Available to borrowers in qualifying rural areas, the U.S. Department of Agriculture (USDA) may not require a down payment. However, income requirements apply along with annual mortgage insurance fees.

- Construction loans: Finance building a new home from the ground up with multiple draws to minimize borrowing costs. You may be able to convert this loan into a permanent mortgage once your house is move-in ready.

- Interest-only mortgage: Only pay interest during the initial portion of the repayment period. Principal and interest payments are due after the introductory period ends.

- Balloon mortgage: A loan with low ongoing monthly payments yet requires a significant final lump-sum payment. The Consumer Financial Protection Bureau rarely considers this loan type a qualified mortgage due to its high level of risk.

- Piggyback loan: A second mortgage that helps cover the down payment so the loan-to-value ratio is 80% or lower for the first mortgage. As a result, the buyer doesn’t need to make private mortgage insurance premiums.

- Home equity loan: This is a second mortgage for existing homeowners to receive a lump-sum distribution of their available equity. It’s an alternative to a cash-out refinance as it leaves the original mortgage intact and has a fixed interest rate.

- Home equity line of credit (HELOC): Current homeowners can tap their available equity with multiple draws as cash is needed. Interest-only payments are required during the draw period and principal payments start when the draw period closes and the repayment period begins. HELOC rates are almost always variable.

First-time homebuyer tip: You might be eligible for reduced down payment requirements of 3% or less on conventional loans. These specialized programs may not require private mortgage insurance (PMI) although your interest rate can be higher than putting at least 20% down. Lenders and government agencies might also offer down payment or closing cost grants and assistance to first-time homeowners.

How to apply for a mortgage

Following these steps can help you qualify for a home loan:

- Review your credit history. Check your credit score to determine which mortgage programs you can be eligible for initially. Conventional home loans usually require a minimum 620 credit score while government-backed mortgages can be as low as 580 or even 500.

- Collect supporting documentation. Gathering your recent pay stubs, two years of income tax returns, two months of bank statements and government-issued ID cards can help you save time when it’s time to apply.

- Compare lenders. Applying for mortgage preapproval requires a hard credit check but you can receive a personalized rate and loan limit for conventional and government-backed programs. Get rate quotes from several lenders to find the best offer.

- Apply for a loan. After a seller accepts your offer, it’s time to apply for a mortgage through your desired lender. A loan officer can help compare your loan and down payment options to get the best rate and monthly payment.

- Complete the underwriting process. The application-to-close process usually takes from 30 to 45 days. During this time, the lender will review your credit and income history and request supporting documentation as needed. Your new home will also be appraised to calculate your loan-to-value ratio and minimum down payment.

- Sign closing documents. At the loan closing, you will sign the final documents to confirm the repayment agreement. Any upfront fees are due at this time. You can move into your home and will start making monthly payments.

Tips for choosing the best mortgage

These practices can help you find the best mortgage lender and loan type:

- Know how much house you can afford. A home affordability calculator estimates the monthly payment you can comfortably afford. Having a maximum purchase price in mind can also make it easier to get preapproval if you can find a house for less than your maximum borrowing power.

- Compare home loan options. Your credit score, annual income and geographic area may help you qualify for government-backed FHA, VA or USDA loans. These loans can have more lenient borrower requirements than conventional loans.

- Consider down payment requirements. First-time homebuyers may only have to put 5% down or less. These loans can be easier to qualify for than a traditional conventional loan, but you may consider a 20% down payment to avoid private mortgage insurance.

- Choose a mortgage term. Opting for a 15-year or a 20-year fixed-rate mortgage instead of a 30-year term lets you qualify for a lower interest rate if you can afford a higher loan payment and pay less interest overall. Be sure to estimate your monthly mortgage escrow payments to calculate your housing costs accurately.

- Compare several lenders. Prequalify with multiple lenders to compare mortgage rates and fees which can vary widely for a similar loan amount and repayment period. In addition to your upfront closing costs and monthly payment, see if the lender offers other perks such as waived lender fees if you refinance later.

Frequently asked questions (FAQs)

Conventional loans require a minimum 620 credit score. Depending on the down payment amount, FHA loans require a 500 or 580 credit score.

Regarding VA-backed home loans, the Department of Veterans Affairs doesn’t have a minimum score requirement, although lenders typically require a score above 620.

Similarly, the USDA loan program doesn’t have credit score requirements, although many USDA lenders insist upon having a minimum 640 score to apply.

Mortgage lenders may be able to deliver a lower mortgage rate and fees along with faster closing speeds as they tend to be online-only and minimize costs. However, banks can be better when you have an existing relationship or you qualify for specialized programs to receive financing and discounts that direct lenders are less likely to offer.

Finding the best rates depends on several factors, including your banking relationship and if you want to qualify for a specialized loan program, such as a first-time homebuyer program or one with a low down payment.

Online mortgage lenders are more likely to charge lower lender fees for traditional home loans than brick-and-mortar locations as they have fewer operating expenses. However, you should still compare your loan APR and total estimated borrowing costs from multiple lenders.

Keep in mind that going with a big bank can be the better option if you’re eligible for a specialty program that offers low down payment requirements or income-based homebuyer grants. You may also qualify for a relationship discount if you’re a current banking customer.

Find out more about how to get a mortgage with a competitive rate.

FHA loans can be the easiest to qualify for as the minimum credit score is either 500 or 580 and has flexible down payment requirements. The down payment is 3.5% with a minimum 580 credit score and 10% with a score as low as 500.

A 30-year fixed interest rate could be a good option for many borrowers as it offers the lowest monthly payment and secures the same rate for the longest period. However, this term usually has higher interest rates than shorter loan terms and more lifetime interest costs.

If you can afford a higher monthly payment, a 15-year term can be an excellent option since you can qualify for a lower rate. You’ll also pay off your mortgage in half the time compared to a 30-year mortgage.

They can be. You can reach out to your lender and ask about reducing:

- Application fees

- Discount points

- Origination fees

- Title insurance

- Underwriting fees

However, choosing a lender with lower origination fees and discount points in the first place can be more effective than asking for a fee reduction during the mortgage application process.

If you’re buying a home, see if the seller will pay a share of the closing costs. Your realtor can assist with this negotiation process.

Editor’s Note: This article contains updated information from previously published stories:

- Mortgage rates jump to a new high for 2016

- Homeowners hurt by COVID-19 can delay mortgage payments, but some say they’re anxious and confused about the real cost

- More than 6M households missed their rent or mortgage payment in September

- Mortgage rates jump again for 2nd week and hit 2017 highs

- Government shutdown 2019: Homebuyers with USDA mortgages can’t close on house sales

- Low down on new low down conventional loans

- Should you get a reverse mortgage? The reasons you should or shouldn’t

- Mortgage delinquencies surge by 1.6M in April, the biggest monthly jump ever

- Here’s how the Fed’s surprise interest-rate cut affects mortgages, credit cards and home equity lines

- Average 30-year mortgage rate jumps to 4.4%

- Mortgage interest rates 2018: Rates hit 7-year high, slow home sales

- Mortgage rates on 30-year home loan hit 5 percent, a nearly 8-year high

- Average 30-year mortgage rate tops 4%

- Mortgage rates: Nowhere to go but up?

- Mortgage rates dip as taper fears subside

- Mortgage applications surge on refinances as rates hit 21-month low

- Will mortgage rates keep dropping? Homeowners and buyers benefit from lower interest rates

- Average 30-year mortgage rate drops to 4.22%

- Mortgage closing costs are on the way up

- Amid surging COVID-19, Fed could take steps to lower mortgage rates, boost economy

Blueprint is an independent publisher and comparison service, not an investment advisor. The information provided is for educational purposes only and we encourage you to seek personalized advice from qualified professionals regarding specific financial decisions. Past performance is not indicative of future results.

Blueprint has an advertiser disclosure policy. The opinions, analyses, reviews or recommendations expressed in this article are those of the Blueprint editorial staff alone. Blueprint adheres to strict editorial integrity standards. The information is accurate as of the publish date, but always check the provider’s website for the most current information.