Best personal loans of April 2024

“Verified by an expert” means that this article has been thoroughly reviewed and evaluated for accuracy.

BLUEPRINT

Updated 6:36 a.m. UTC April 16, 2024

Editorial Note: Blueprint may earn a commission from affiliate partner links featured here on our site. This commission does not influence our editors' opinions or evaluations. Please view our full advertiser disclosure policy.

You can use a personal loan to cover almost any expense up to $100,000, depending on the lender. Maybe you need to pay off your credit cards or cover medical expenses. Or maybe an emergency pops up and you need extra cash.

Typically, you’ll need good credit to get approved, but it’s also possible to get a personal loan with bad credit. Some lenders accept scores below 600, and several allow co-signers or joint applicants.

Before applying for a personal loan, it’s important to compare your options. To make it easier, we’ve done the research for you. Here are the best personal loans of 2024.

Best personal loans

- SoFi: Best overall.

- LendingPoint: Best for fair credit.

- Upgrade: Best for poor credit.

- Prosper: Best peer-to-peer lender.

- Axos Bank: Best for excellent credit.

- LightStream: Best for fast funding.

- Discover: Best for good credit.

- Avant: Best for customer support.

- U.S. Bank: Best for repayment term variety.

- Oportun: Best for building credit.

- Upstart: Best for thin credit.

- Citibank: Best for rate discounts.

Why trust our personal loan experts

Our team of experts evaluated hundreds of personal loan products and analyzed thousands of data points to help you find the best fit for your situation. We use a data-driven methodology to determine each rating. Advertisers do not influence our editorial content. You can read more about our methodology below.

- 40 personal loan lenders reviewed.

- 640 data points analyzed.

- 6-stage fact-checking process.

Our top picks for personal loans in 2024

Compare the best personal loan lenders

| INTEREST RATES | LOAN AMOUNTS | REPAYMENT TERMS (YEARS) | TIME TO FUND (AFTER APPROVAL) | |

|---|---|---|---|---|

SoFi

| 8.99% to 29.49%

| $5,000 to $100,000

| 2 to 7

| As soon as the same day

|

LendingPoint

| 7.99% to 35.99%

| $2,000 to $36,500

| 2 to 6

| As soon as the next business day

|

Upgrade

| 8.49% to 35.99%

| $1,000 to $50,000

| 2 to 7

| Within 1 business day

|

Prosper

| 6.99% to 35.99%

| $2,000 to $50,000

| 2 to 5

| Within 1 business day

|

Axos Bank

| 11.79% to 20.84%

| $5,000 to $50,000

| 3 to 6

| As soon as the same day

|

LightStream

| 7.49% to 25.99%

| $5,000 to $100,000

| 2 to 7

(up to 12 for some loan types)

| As soon as the same day

|

Discover

| 7.99% to 24.99%

| $2,500 to $40,000

| 3 to 7

| As soon as 1 business day

|

Avant

| 9.95% to 35.99%

| $2,000 to $35,000

| 1 to 5

| As soon as the next business day

|

U.S. Bank

| 8.74% to 24.99%

| $1,000 to $50,000

($25,000 maximum for non-U.S. Bank customers)

| 1 to 7

(5-year maximum for non-U.S. Bank customers)

| 1 to 4 business days

|

Oportun

| 34.95% to 35.99%

| $300 to $18,500

(depending on loan type)

| 1 to 5.33

| As soon as the same day

|

Upstart

| 7.8% to 35.99%

| $1,000 to $50,000

| 3 or 5

| As fast as 1 business day

|

Citibank

| 10.49% to 19.49%

| $2,000 to $30,000

| 1 to 5

| As soon as the same day with an existing Citi account

|

All interest rates are current and include discounts as applicable as of April 8, 2024.

Methodology

Our expert writers and editors have reviewed and researched multiple lenders to help you find the best personal loan lender for your situation. Out of all the lenders considered, the ones that made our list excelled in areas across the following categories (with weightings):

Within each major category, we considered several characteristics, including APR ranges, loan amounts, maximum repayment terms, lender discounts, late payment and prepayment penalties, minimum credit score requirements and funding time as well as co-signer or co-borrower acceptance. We also evaluated each lender’s customer support contact options and availability, as well as real customer reviews.

What can I use a personal loan for?

You can use a personal loan for almost any purpose — including big expenses like RVs, pools, home improvement, a wedding and more. Small personal loans are also available from certain lenders and can be used to pay for things like medical or veterinary bills.

Pros and cons of taking out a personal loan

| Pros | Cons |

|---|---|

Can borrow up to $100,000 from some lenders.

| Might have higher rates than other options (like home equity loans or home equity lines of credit (HELOCs).

|

Could have up to seven years to repay the loan (depending on lender).

| Some lenders charge origination and late payment fees.

|

Could get your money the same day or next day (depending on lender).

| Monthly payments could be high, depending on how much you borrow.

|

Personal loan rates forecast for 2024

The Federal Reserve has increased the federal funds rate 11 times since March 2022 in efforts to reduce inflation. Lenders responded by raising rates on consumer loan products like personal loans. As a result, personal loan rates have been inarguably high.

But the Federal Open Market Committee (FOMC) has declined to hike rates any further during its first two meetings in 2024. Federal Reserve Chair Jerome Powell has also indicated that rates could be cut in 2024 if inflation continues to decline toward the Fed’s 2% target rate. In March 2024, the FOMC projected the federal funds rate will fall to a median of 4.6% by the end of the year.

If inflation rates decline and the federal funds rate drops, personal loan rates could follow —but that’s a big “if.” On top of the federal funds rate, borrower demand is another key factor that plays into the trajectory of personal loan rates. While the number of personal loan originations increased from 18.6 million in 2021 to 22.1 million in 2022, they fell to 19.3 million 2023, according to data from TransUnion. If borrower demand for these loans declines in 2024, lenders might opt to reduce rates to attract customers.

Save money on borrowing costs: Compare the best personal loan rates

How to get a personal loan

Generally, you’ll need to meet certain requirements to get approved for a personal loan. Though these requirements can vary by lender, here’s what you typically need:

- Know how much you need to borrow. Before deciding to take out a loan at all, decide on the amount. It’s best to only take out what you need — otherwise you could over borrow and get stuck in a cycle of debt.

- Review your credit. Before applying for a loan, you should know what your credit score is and what’s on your report. Most lenders require a good credit score for approval, however there are some lenders that work with bad credit. When you review your credit report, be careful to note any possible errors or items you should address. Fixing any issues before you apply could give you a better score to work with. You can also improve your credit by paying your monthly bills on time and paying down your total debt as much as possible.

- Compare multiple lenders. Once you’ve decided on the type of lender, you still should compare multiple options. Keep an eye on the interest rate offered, any fees that might add to the cost of the loan and the repayment options available.

- Prepare your documents and apply. The lender will want to verify your identity, place of residence and income. Typically, you’ll need to have your driver’s license or passport, proof of address, pay stubs, bank statements and tax returns on hand. You can fill out the application on the lender’s website (or in person if you chose to go to a physical location). Once submitted, just wait for a response to your application.

Tip: You can get a personal loan through banks, credit unions and online lenders. However, the best places to get a personal loan will depend on your situation. A bank or credit union might be the right choice if you already have a relationship established as some offer rate discounts to current customers.

But if you’re comfortable applying online, an online lender might offer lower rates than those with physical branches — and their application process is typically faster.

Personal loan requirements

Most personal loans are unsecured, meaning they don’t require any form of collateral to secure the loan — like a vehicle or savings account. But you’ll still need to meet certain requirements to get approved for a personal loan. Though these requirements can vary by lender, here’s what you typically need:

- Good credit: Some lenders may require that you have good credit, or a credit score over 670, to qualify for a personal loan. Others may have more flexible credit score requirements.

- Verifiable annual income: You’ll likely need to meet certain annual income requirements to get approved. Income requirements vary significantly by lender.

- Low debt-to-income (DTI) ratio: Lenders typically consider your DTI ratio, which measures your total monthly income against your monthly debts, when determining whether to approve you for a loan. Generally, a DTI below 36% is considered good, but the lower your DTI, the better.

- Live in an eligible location: Some lenders only operate in certain states, so it’s essential to find one that lends where you live.

How to increase your likelihood of approval

If you’re concerned that you won’t qualify for a personal loan, there are certain things you can do to increase your chances:

- Use a co-signer or joint borrower. One strategy worth considering is to apply for a personal loan with a co-signer or joint borrower (co-borrower). Many of the best companies for personal loans offer the option to use a joint borrower for personal loans, but fewer let you apply with a co-signer. When you use a creditworthy co-borrower or co-signer, your lender will review their credit history in addition to yours — making you more likely to qualify.

- Seek alternative funding. You could ask someone you trust, like a friend or family member, for a loan or even consider applying through a peer-to-peer (P2P) lending platform like Prosper to get a P2P loan.

- Improve your credit. If you have some time before you’ll need funds, you could work on improving your credit before applying. Things like paying down existing debt, setting up monthly automatic bill payments and increasing your income could all help boost your credit score.

Find out why improving your credit can help: 5 benefits of a good credit score

How to choose the best personal loan for you

Overall, the best personal for you is one with a low rate, reasonable monthly payment and minimal fees. But here are some things to keep in mind when deciding on a loan:

- Loan purpose: Whether you want to take out a loan to cover medical bills or consolidate debt, some loans cater to specific loan uses. For example, if you need to consolidate multiple debts, finding a lender who specializes in debt consolidation and can pay off multiple creditors directly might be ideal.

- Amount: Once you know how much you need to borrow, compare loan amounts of different lenders to find one that will allow you to borrow as little (or as much) as you need.

- Interest rate: The lower the interest rate, the less interest you will have to pay over the life of the loan. So, it’s always important to find a lender that offers a reasonable and affordable rate.

- Fees: Paying interest isn’t the only cost of a personal loan. Some lenders might charge origination fees, prepayment penalties or late payment fees. Make sure you factor all of these in when looking at the total cost of the loan you’re considering.

- Monthly payment: A low rate, low cost loan is ideal — but not if it means your monthly payment isn’t manageable. Use a personal loan calculator to estimate your monthly payments so you’re not surprised when it comes time for that first monthly payment and it’s not something you can reasonably afford.

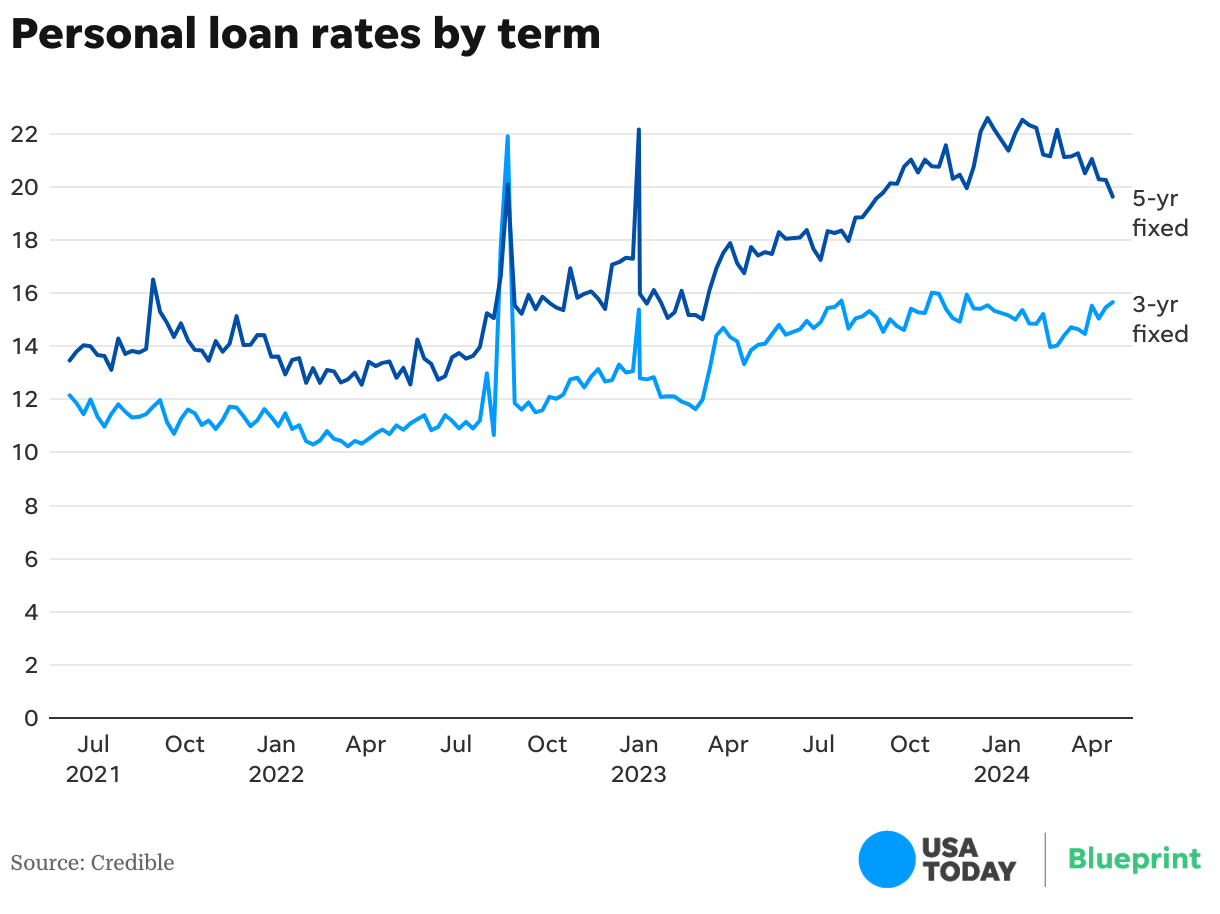

Current personal loan interest rates

Personal loan interest rates can vary significantly depending on the lender. For instance, some lenders might offer APRs as low as 6.7% or as high as 35.99% The rate you receive will depend upon your overall creditworthiness and other factors.

Here are the current average interest rates for three- and five-year personal loans:

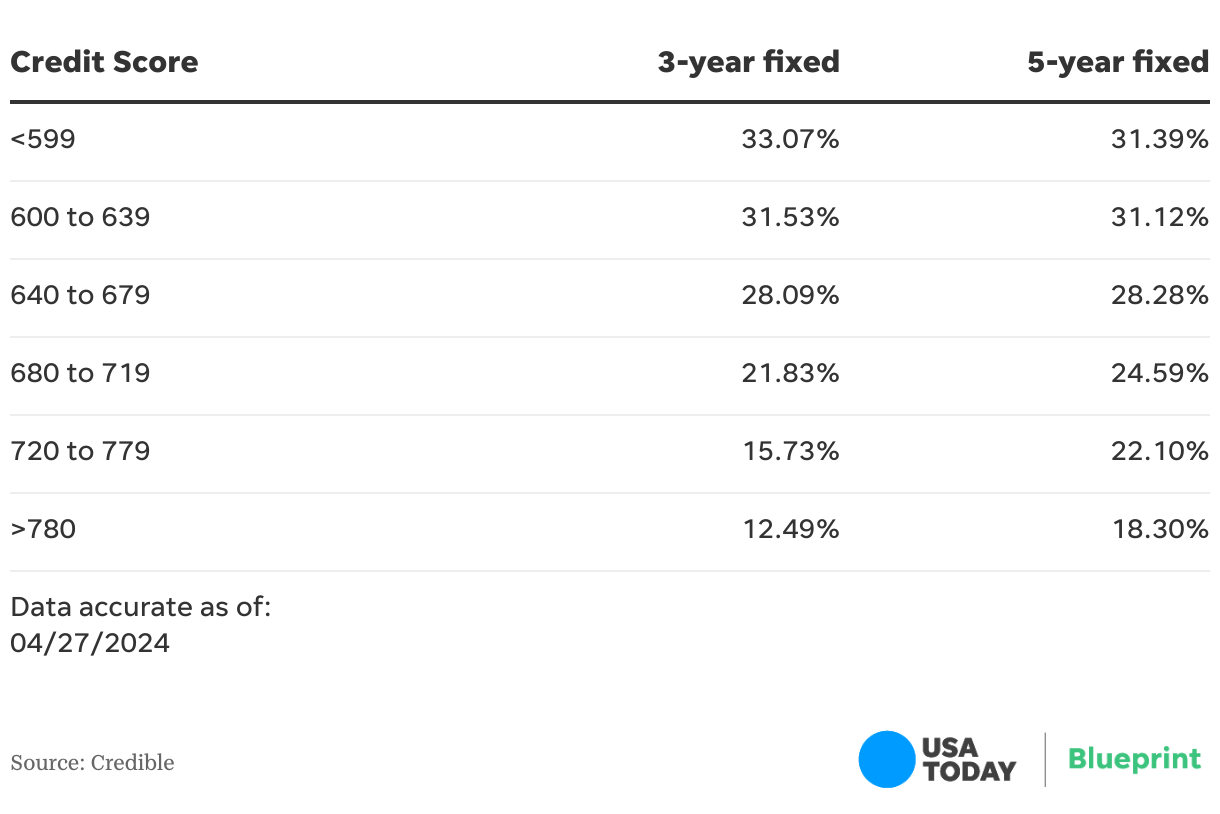

Personal loan rates by credit score

Frequently asked questions (FAQs)

While exact credit score requirements vary by lender, you’ll generally need good to excellent credit to qualify for a personal loan. A good credit score is usually considered to be 670 or higher.

There are also several lenders that work with borrowers who have lower credit scores. These include some of our picks for the best loan companies, like Upgrade and Upstart. However, keep in mind that bad credit loans typically come with higher interest rates compared to those offered to borrowers with good credit.

Most personal loan lenders look for good to excellent credit.

“That’s because most personal loans are unsecured, which means you won’t need to put up collateral … if you can’t or won’t pay back the debt,” says Leslie Tayne, founder and head attorney at Tayne Law Group. “The lender needs reasonable assurance that they can trust you to meet your financial obligation, so they set qualification criteria high.”

While you’ll have fewer options for personal loans with bad credit, certain lenders offer personal loans for bad credit. In general, though, you’ll want to avoid payday loans and loans with very high APRs, as those can be difficult or near impossible to pay off.

In general, the quickest way to get a personal loan is with an online lender that offers same- or next-day funding, such as LightStream. While traditional banks and credit unions sometimes provide fast funding, online lenders typically offer speedier application and funding times.

Interest rates on personal loans fluctuate often, and different lenders offer varying APR ranges. In general, though, a rate that’s below the Fed’s average of 11.49% for a two-year personal loan may be considered a good rate. It’s essential to compare personal loan rates from different lenders to find an affordable loan.

Both online lenders and banks offer personal loans, but the ideal option for you depends on your situation. If you prefer to apply in person, a local bank or credit union might be the right choice. But if you’re comfortable applying online, an online lender might offer lower rates than those with physical branches — and their application process is typically faster.

Editor’s Note: This article contains updated information from previously published stories:

- Young adults turn to personal loans for debt, wedding and moving expenses

- Behind on bills? A new personal loan will help, TransUnion study says

- How should you compare personal loans? Don't just look at interest rates

- 5 times when getting a personal loan is a big mistake

- Black Friday 2018: Should you get a personal loan for holiday shopping this year?

Blueprint is an independent publisher and comparison service, not an investment advisor. The information provided is for educational purposes only and we encourage you to seek personalized advice from qualified professionals regarding specific financial decisions. Past performance is not indicative of future results.

Blueprint has an advertiser disclosure policy. The opinions, analyses, reviews or recommendations expressed in this article are those of the Blueprint editorial staff alone. Blueprint adheres to strict editorial integrity standards. The information is accurate as of the publish date, but always check the provider’s website for the most current information.